The decline in US Treasury bond yields on the back of a slowdown in US employment was the primary driver behind the USDJPY pair’s nosedive. However, this is not the only positive development for the yen. Let’s discuss this topic and make a trading plan.

The article covers the following subjects:

Highlights and key points

- The USDJPY is falling due to the decline in US Treasury yields.

- Capital repatriation to Japan supports the yen.

- The BoJ may raise rates faster than expected.

- The USDJPY will likely continue sliding to at least 139.

Quarterly fundamental forecast for Japanese yen

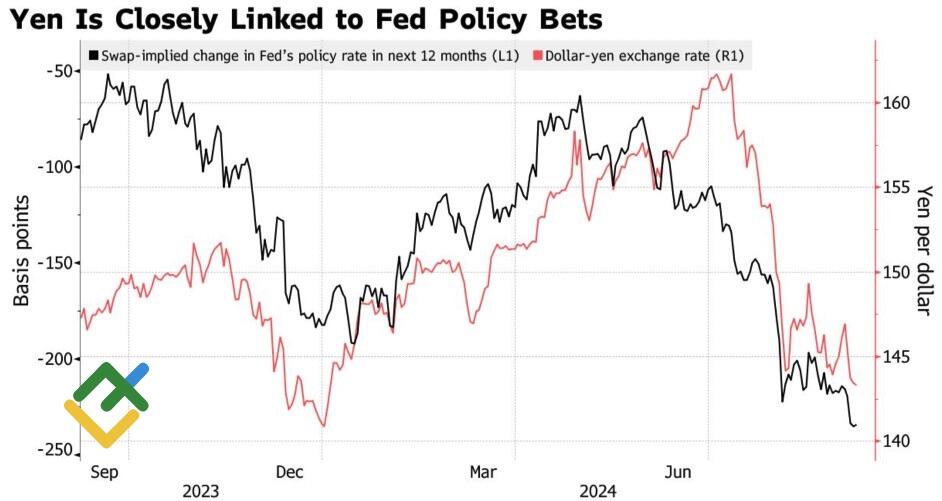

Should key economic indicators deviate from expectations, the Japanese yen is likely to be a market focus. This is the prevailing view in the Forex market, and it was amply validated following the release of the US employment data. In contrast to other US dollar pairs, which experienced a roller coaster ride, the USDJPY pair showcased a consistent downward movement. Its decline was supported by the 10-year US Treasury yield reaching a 15-month low.

It would be incorrect to assume that the yen is not reacting to the anticipated scale of the Fed’s monetary expansion. In fact, it is. However, USDJPY traders should consider other factors, such as fears of an impending recession in the US and the repatriation of capital to Japan amid the BoJ’s monetary policy normalization. These factors affect the rates of the US debt market, which has a significant impact on the value of the Japanese currency.

USDJPY rate and expected scope of the Fed’s monetary expansion

Source: Bloomberg.

In this regard, the inversion of the US yield curve and a forecast that the Government Pension Investment Fund (GPIF), the largest public fund investor in Japan, would increase the share of Japanese equities in its portfolio were equally influential in pushing the USDJPY pair down. This was on par with the impact of rumors surrounding the Bank of Japan’s (BoJ) continuation of its monetary policy stance. According to a recent Bloomberg survey, nearly half of the 21 experts surveyed believe that GPIF, which has $1.75 trillion in assets, will increase its weighting in local equity securities from the current 25% starting in April. The repatriation of capital could accelerate the USDJPY‘s plunge.

It is possible that the normalization of monetary policy by the Bank of Japan could trigger market turbulence soon. The events of Black Monday on August 5 served as a kind of dress rehearsal, but it would be unwise to rule out the possibility of further turbulence in the future. Former BoJ official Tsutomu Watanabe believes that the regulator should establish effective communication with the markets and clearly indicate its future actions. In contrast to the Bloomberg experts, who anticipate a single monetary restriction in 2024, Watanabe anticipates two.

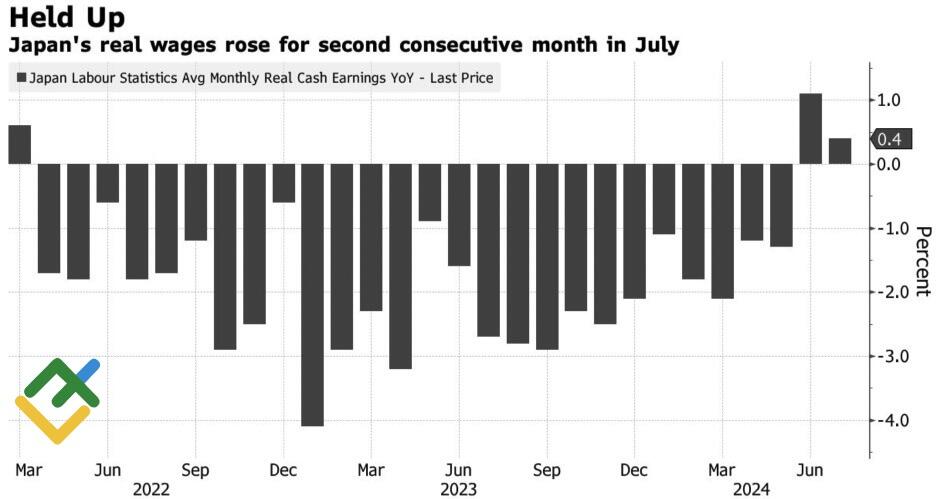

Indeed, there are numerous reasons for the Bank of Japan to take more decisive action. Real wages in July rose for the second consecutive month, indicating that further GDP recovery is likely. In the second quarter, the country’s gross domestic product saw a 2.9% expansion, and this trend is expected to continue.

Japan’s real wages

Source: Bloomberg.

A robust economy cannot coexist with weak inflation, so consumer prices in Japan will remain above the 2% target for a longer period than projected. This necessitates an increase in the overnight rate to combat inflation.

Quarterly USDJPY trading plan

Therefore, the USDJPY pair’s downtrend persists due to divergence in monetary policy and economic growth between the US and Japan. Bearish targets of 139 and 133.5 remain relevant. However, the pair may enter a consolidation phase within the 142-145 range soon. Thus, one can also sell the pair during price spikes.

Price chart of USDJPY in real time mode

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2004/39/EC.

{{value}} ( {{count}} {{title}} )

This post is originally published on LITEFINANCE.