The heightened probability of an overnight rate hike by the Bank of Japan and the waning influence of the Trump trade have allowed USDJPY bears to return to the market. Nevertheless, it is crucial to ascertain whether the US dollar’s weakness is merely temporary. Let’s discuss this topic and make a trading plan.

The article covers the following subjects:

Major Takeaways

- The US may prefer negotiations to trade duties.

- The Bank of Japan will make decisions depending on incoming data.

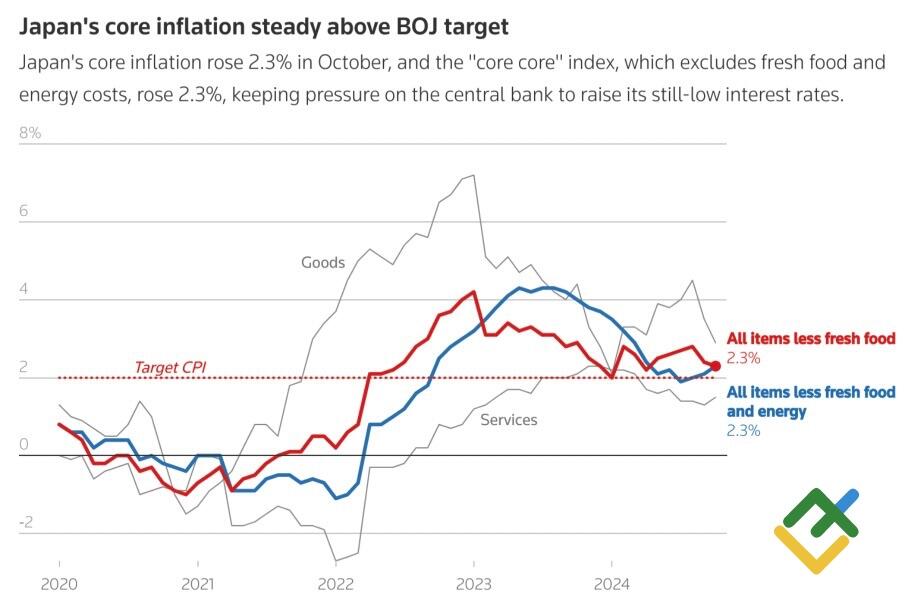

- Inflation in Japan is accelerating.

- The USDJPY pair may consolidate in the 152–156.5 range.

Weekly Fundamental Forecast for Yen

As a rule, a currency has to retreat once its advantages start to wane. The MLIV Pulse survey revealed that approximately 70% of respondents believe that the US dollar would continue to strengthen against major world currencies over the next month, driven by rising Treasury yields and robust demand for safe-haven assets. Meanwhile, the appointment of Scott Bessent as US Treasury Secretary has prompted USDJPY bulls to adopt a more cautious approach against lower US debt market rates and fears of trade wars.

The hedge fund manager has previously stated that Donald Trump’s proposed import duties were excessive. Bessent believes in pursuing negotiations at gunpoint, where countries are compelled to renegotiate trade terms under the threat of tariffs in order to align their interests with those of the US. Scott Bessent’s lack of experience has led to concerns about the potential impact on the economy and a decline in the yields of Treasuries. Against this backdrop, USDJPY bears managed to take advantage of this situation.

In addition, the acceleration of core inflation in Japan in October from 2.1% to 2.3% and Reuters experts’ forecasts of an increase in consumer price growth in Tokyo from 1.8% to 2.1% in November indicate that the BoJ may continue the normalization cycle as early as December.

Japan’s Inflation Change

Source: Reuters.

This viewpoint was expressed by 29 out of 56 Bloomberg experts, representing 56% of the total. In October, 49% of respondents voted in favor of raising the overnight rate by 25 bps to 0.5% by the end of 2024. Kazuo Ueda stressed that the Bank of Japan’s decisions would be data-driven, that the Board of Governors planned to adjust its forecasts in line with developments at each meeting, and that only the announcement of Donald Trump’s policies by the new administration would force the BoJ to adjust its forecasts.

In theory, an increase in trade tariffs should initially spur inflation in the US due to the impact on import prices. However, this will subsequently result in a weaker economy and a slowing of CPI. As anticipated, annual inflation expectations are rising, while the longer-term indicator is not yet showing the same trend. Should trade wars prove less disruptive than estimated by Scott Besent, US PCE may not accelerate. If this occurs, the Fed will continue to cut rates, allowing USDJPY bears to regain the upper hand.

Until the end of the year, it will remain unclear which of Donald Trump’s election promises will be fulfilled and which will not. This creates an environment conducive to a Trump trade retreat and consolidation of USD pairs. Investors’ attention will shift to central banks and macroeconomic statistics. In this regard, the publication of the minutes of the October FOMC meeting and the release of inflation data in Tokyo will likely drive the USDJPY pair’s quotes.

Weekly USDJPY Trading Plan

In light of the prevailing circumstances, the USDJPY pair will likely consolidate within the range of 152-156.5. A strategic approach would be to sell the USDJPY pair on growth towards the upper boundary of the range and buy it if the quotes drop to the lower boundary.

Price chart of USDJPY in real time mode

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2004/39/EC.

{{value}} ( {{count}} {{title}} )

This post is originally published on LITEFINANCE.