The most prominent BoJ hawk’s proposal to raise the overnight rate to 1% and Japan’s positive economic statistics have triggered a sell-off in the USDJPY pair. However, it is important to question the assumptions of bears and understand the factors behind their positions. Let’s discuss this topic and make a trading plan.

The article covers the following subjects:

Major Takeaways

- The BoJ overnight rate may rise to 1%.

- Wages in Japan have posted the biggest gains since 1997.

- The yen’s trajectory depends on the US inflation report.

- Long trades can be opened if the USDJPY pair breaks through the resistance level of 152.45.

Weekly Fundamental Forecast for Yen

The most recent data show a notable increase in Japan’s nominal cash earnings, marking the fastest growth since 1997. This development, coupled with a statement by the Bank of Japan official Naoki Tamura emphasizing the need to raise the overnight rate to 1%, triggered a significant decline in the USDJPY exchange rate, reaching a two-month low. The yen has emerged as a leader in the G10 currency group, with Barclays reporting that it is the currency being purchased more than the US dollar is being sold.

Nominal Wages in Japan

Source: Bloomberg.

The USDJPY’s decline was fueled by the speech of US Treasury Secretary Scott Bessent, who indicated that Donald Trump would not interfere in the Fed’s monetary policy. The President wants the 10-year Treasury bond yields to fall, and given the pair’s increased sensitivity to the rates of the US debt market, a fall in response to such rhetoric seems logical.

However, according to Jupiter Asset Management, the primary factor contributing to the yen’s strengthening is the domestic nature of inflation in Japan, which is not imported. Rising wages, cash incomes, and the surge in the core CPI to 3% support this view. The BoJ is more likely to raise rates than reduce them. This underscores the success of the yen, especially in light of the substantial monetary expansion by other central banks.

The absence of duties on imported Japanese cars after a meeting between Prime Minister Shigeru Ishiba and US President Donald Trump is also a contributing factor. Tokyo has proposed increased US LNG purchases and increased investment in the US economy by Toyota Motor and Isuzu Motors as potential incentives. The effectiveness of these measures in satisfying the White House’s expectations remains to be seen.

I would be remiss not to mention one additional point. Naoki Tamura, regarded as the most hawkish member of the Policy Board, has indicated a potential rate increase in the 2025/2026 fiscal year, aligning with the previous pace of two acts of monetary expansion in 12 months. This dynamic contributed to the weakening of the yen in 2024, coinciding with a cut in the federal funds rate. In 2025, the Fed is expected to maintain a pause in rate hikes. This prompts the question of why the USDJPY exchange rate should not rise.

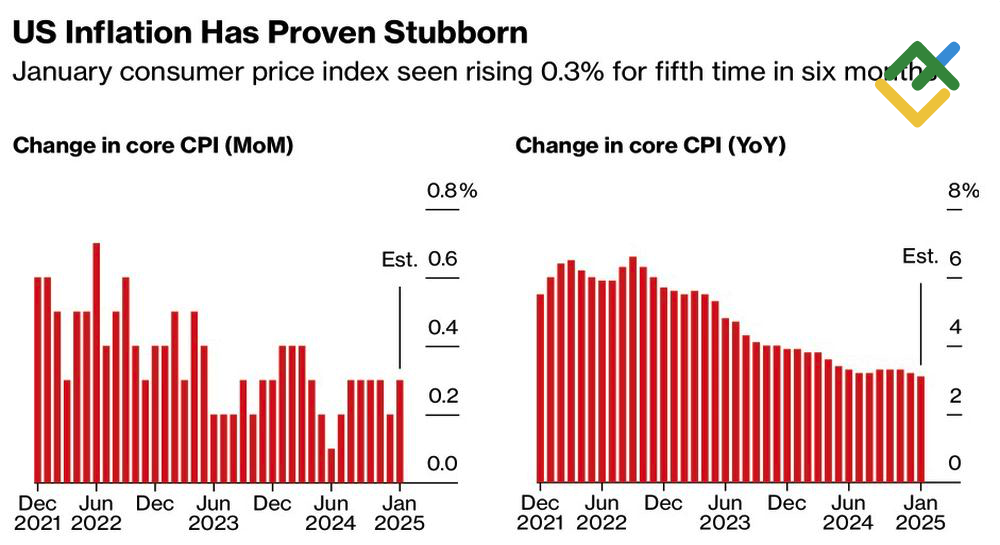

US Inflation Change

Source: Bloomberg.

US inflation statistics have the potential to trigger a rally in the pair. Current projections indicate that prices will remain close to the 3% mark. However, BNP Paribas notes that in 13 of the last 14 reports for January, actual data exceeded forecasts. Should this occur, the derivatives market will likely increase the odds of a monetary expansion by the Fed. In addition, US Treasury yields are expected to rise, and the US dollar is likely to strengthen.

Weekly USDJPY Trading Plan

President Trump’s commitment to addressing trade imbalances will likely significantly hurt the Japanese yen. Concurrently, the recovery of US debt market rates, fueled by US inflation acceleration in January, will allow traders to open long positions on the USDJPY pair once it exceeds the 152.45 resistance level.

This forecast is based on the analysis of fundamental factors, including official statements from financial institutions and regulators, various geopolitical and economic developments, and statistical data. Historical market data are also considered.

Price chart of USDJPY in real time mode

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance broker. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2014/65/EU.

According to copyright law, this article is considered intellectual property, which includes a prohibition on copying and distributing it without consent.

{{value}} ( {{count}} {{title}} )

This post is originally published on LITEFINANCE.