Germany is grappling with an escalating wave of

digital banking fraud, driven by a surge in phishing attacks, investment scams,

and emerging tactics like QR code phishing.

Unlike other European nations, where fraud trends are

shifting, phishing remains Germany’s primary threat, with cases rising 4.8% in

the past year, according to research by BioCatch.

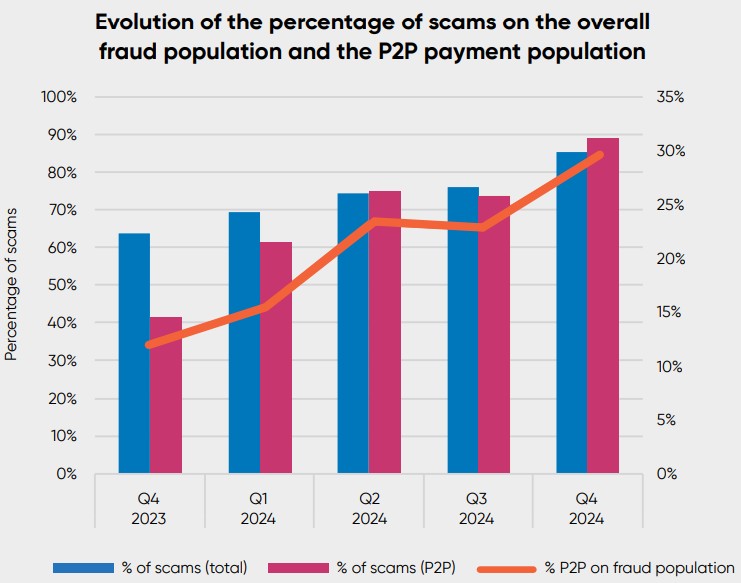

With the EU‘s Instant Payments Regulation (IPR) now in

effect, fraud risks could intensify as criminals exploit faster transactions to

deceive consumers and financial institutions.

Phishing, Social Engineering, and a Trust Deficit

Phishing scams continue to dominate Germany’s fraud

landscape, leading to financial losses and diminishing trust in online banking.

According to the research, Germans have collectively lost €267 billion to

phishing attacks, with 69% of incidents occurring through digital channels.

This has made consumers increasingly wary of online

transactions, with 32% viewing AI as a threat rather than an opportunity. Unlike other European countries where banks often

cover losses, German victims must prove they were not negligent, making it

harder to reclaim stolen funds.

Additionally, the rise of QR code phishing, or

“quishing,” has further complicated the landscape. Fraudsters have

reportedly been placing fake QR codes on parking meters, EV charging stations,

and even bank notifications to steal user credentials and inject malware into

unsuspecting victims’ devices.

A staggering 43% of social media users in Germany have

invested in digital assets, often relying on influencers rather than

professional advisors. Despite their confidence, younger investors are highly

vulnerable. While 55% of Gen Z and Millennials believe they won’t be scammed,

they now account for 72% of all scam victims.

However, financial losses remain higher among older

generations, with Baby Boomers losing an average of €18,000 per scam compared

to just €400 for Gen Z victims.

Improved Transaction Speeds and Fraud

The EU’s Payment Services Directive 3 (PSD3) and the

Instant Payments Regulation (IPR) have introduced significant changes to

banking security. Under IPR, payment service providers must process and confirm

euro-denominated instant payments within 10 seconds.

PSD3 aims to strengthen consumer protections by

enhancing Strong Customer Authentication (SCA) requirements, improving Open

Banking oversight, and enforcing stricter compliance for financial

institutions.

However, lessons from early adopters like the UK

suggest that such measures may be more effective in preventing errors than

stopping fraud. Criminals are already adapting, using social

engineering tactics to manipulate victims into authorizing transactions.

Germany is grappling with an escalating wave of

digital banking fraud, driven by a surge in phishing attacks, investment scams,

and emerging tactics like QR code phishing.

Unlike other European nations, where fraud trends are

shifting, phishing remains Germany’s primary threat, with cases rising 4.8% in

the past year, according to research by BioCatch.

With the EU‘s Instant Payments Regulation (IPR) now in

effect, fraud risks could intensify as criminals exploit faster transactions to

deceive consumers and financial institutions.

Phishing, Social Engineering, and a Trust Deficit

Phishing scams continue to dominate Germany’s fraud

landscape, leading to financial losses and diminishing trust in online banking.

According to the research, Germans have collectively lost €267 billion to

phishing attacks, with 69% of incidents occurring through digital channels.

This has made consumers increasingly wary of online

transactions, with 32% viewing AI as a threat rather than an opportunity. Unlike other European countries where banks often

cover losses, German victims must prove they were not negligent, making it

harder to reclaim stolen funds.

Additionally, the rise of QR code phishing, or

“quishing,” has further complicated the landscape. Fraudsters have

reportedly been placing fake QR codes on parking meters, EV charging stations,

and even bank notifications to steal user credentials and inject malware into

unsuspecting victims’ devices.

A staggering 43% of social media users in Germany have

invested in digital assets, often relying on influencers rather than

professional advisors. Despite their confidence, younger investors are highly

vulnerable. While 55% of Gen Z and Millennials believe they won’t be scammed,

they now account for 72% of all scam victims.

However, financial losses remain higher among older

generations, with Baby Boomers losing an average of €18,000 per scam compared

to just €400 for Gen Z victims.

Improved Transaction Speeds and Fraud

The EU’s Payment Services Directive 3 (PSD3) and the

Instant Payments Regulation (IPR) have introduced significant changes to

banking security. Under IPR, payment service providers must process and confirm

euro-denominated instant payments within 10 seconds.

PSD3 aims to strengthen consumer protections by

enhancing Strong Customer Authentication (SCA) requirements, improving Open

Banking oversight, and enforcing stricter compliance for financial

institutions.

However, lessons from early adopters like the UK

suggest that such measures may be more effective in preventing errors than

stopping fraud. Criminals are already adapting, using social

engineering tactics to manipulate victims into authorizing transactions.

This post is originally published on FINANCEMAGNATES.