The oil market is still awaiting further developments. Potential factors that could influence the market include Israel’s retaliation against Iran, China’s new fiscal stimulus, and the possible impact of hurricanes in the Gulf of Mexico. This news could lead to an increase in Brent prices. Let’s discuss this topic and make a trading plan.

The article covers the following subjects:

Highlights and key points

- Israel is taking a cautious approach to the situation with Iran.

- Speculation about China’s economic stimulus is influencing oil prices.

- The most probable outcome is a reduction in geopolitical tensions.

- Brent can be sold on a rebound from the resistance levels of $78.3, $79.4, and $82.5 per barrel.

Weekly fundamental forecast for Brent

Buy the rumor, sell the news. This is the strategy the financial markets usually stick to. However, in October, they engaged with this principle to such an extent that it became untenable. Brent bulls are buying rumors regarding Israel’s potential retaliation against Iran and China’s forthcoming fiscal stimulus following the implementation of monetary stimulus, as well as the impending hurricanes approaching the Gulf Coast. The oil market has become a significant arena where geopolitical factors are influencing market fundamentals more than usual. Against this backdrop, North Sea oil is experiencing significant volatility.

At first glance, the market appears to be in a state of equilibrium. Expectations of a military response from Israel against Iran drive the purchase of Brent, while pessimistic forecasts about global supply and demand give grounds for selling. However, even a minor factor can upset the delicate balance in such an environment. As soon as investors did not receive confirmation of China’s new fiscal stimulus, Brent quotes collapsed.

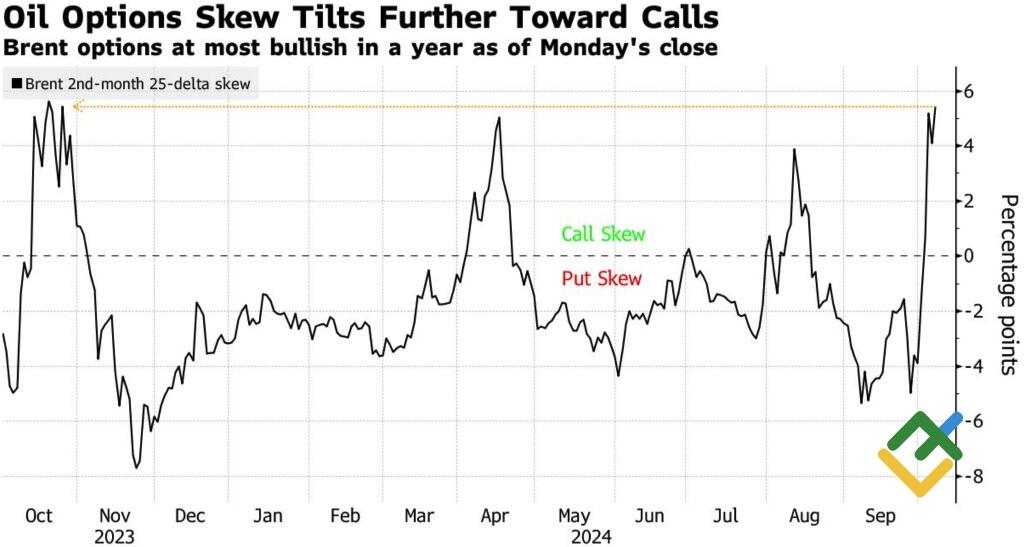

Brent reversal risk

Source: Bloomberg.

Does this indicate that oil will respond in a similar manner to constrained Israeli retaliation? This is not a foregone conclusion. Following this, the markets will be looking to Tehran for a response, so it would be premature to discuss de-escalation and reduction of geopolitical risks at this stage. Notably, the potential for a large-scale armed conflict in the Middle East has not yet been fully reflected in Brent‘s quotes.

It is sufficient to consider a scenario in which Israel launches an attack on the Iranian terminal on Kharg Island, which serves as a primary hub for the transit of 90% of its opponent’s oil supplies. Furthermore, the closure of the Strait of Hormuz should be taken into account. The $90 per barrel forecast by Goldman Sachs will then seem relatively modest.

Nevertheless, it seems that a scenario of such magnitude is still some way off. Investors continue to demonstrate a willingness to make purchases based on market rumors. At the same time, the anticipation of a negative outcome is more concerning than the actual event itself. The longer Israel maintains secrecy regarding its retaliatory measures, the greater the market volatility.

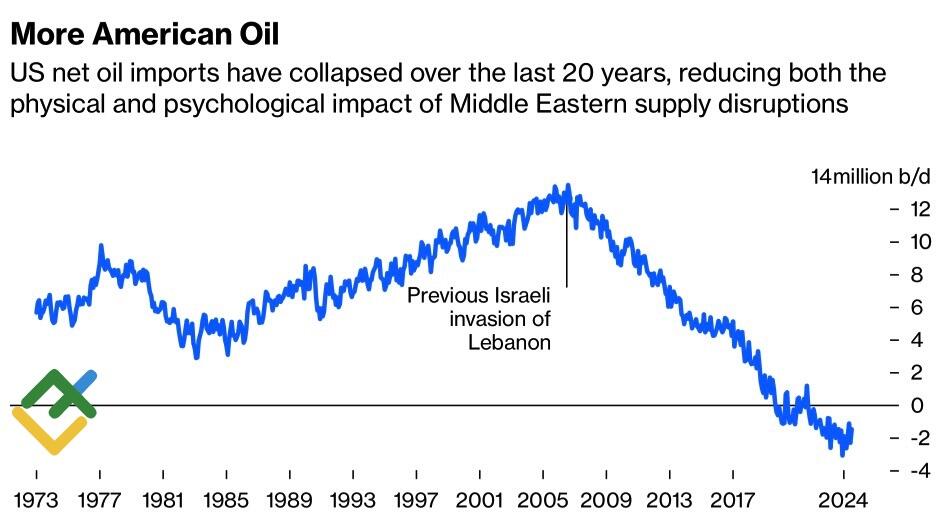

The US is opposed to attacks on oil infrastructure, which would lead to an increase in oil prices and subsequently slow down the global economy. Conversely, while the United States imported 12.5 million barrels per day (b/d) in 2006, it is now a net exporter. Thus, the value of the US dollar is rising in response to the intensifying conflict in the Middle East.

US oil import and export

Source: Bloomberg.

Weekly trading plan for Brent

It seems prudent to assume that any scenario is possible. However, the base-case scenario suggests a de-escalation of the conflict. This will entail limited retaliation by Jerusalem and the absence of retaliatory measures from Tehran. The so-called April scenario will result in significant price fluctuations for Brent. Should prices rebound from the current resistance levels of $78.3, $79.4, and $82.5 per barrel, this would provide an opportunity to sell oil.

Price chart of UKBRENT in real time mode

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2004/39/EC.

{{value}} ( {{count}} {{title}} )

This post is originally published on LITEFINANCE.