Robinhood’s

boss thinks there’s something fundamentally broken about how global capital

markets work. Vlad Tenev, the CEO who built his fortune democratizing stock

trading, now says it’s a “tragedy” that regular investors can’t

access private markets where the real money gets made.

Robinhood Boss Says Wall

Street’s Biggest Secret Is Unfair

Speaking on

Bloomberg

Wealth, Tenev didn’t mince words about what he sees as Wall Street’s

biggest inequity. “A big tragedy is that private markets are where the

bulk of the interesting appreciation and exposure is nowadays,” Robinhood’s Tenev told

host David Rubenstein. “It’s a shame that it’s so difficult to get

exposure in the US.”

The

comments highlight a growing frustration among retail trading platforms as

private companies stay private longer and capture more value before going

public. Companies like SpaceX, OpenAI, and other tech darlings have generated

massive returns for institutional investors while everyday Americans watch from

the sidelines.

What’s

important here, private market investments dramatically outperform public

markets over the long term, generating returns that can be 400-500 basis points

higher annually. The wealth creation difference is staggering – while public

market investors earned 6.6x their money over 25 years, private market

investors generated 19.9x returns according to Cambridge Associates’ comprehensive

data.

The Numbers Don’t Lie

Private

equity has delivered an average annual return of 13.1% over 25 years,

significantly outpacing the S&P 500’s 8.6% return during the same period.

Even more

compelling data comes from MSCI Private Capital Solutions, which shows that

since 2000, private equity has generated a 13% net annualized return compared

to the Russell 3000’s 8% return. This represents outperformance of 486 basis

points annually.

The

illiquidity premium alone adds 2-4% annually to private equity returns over the

long run. This premium compensates investors for giving up the ability to sell

their investments quickly, but the trade-off has proven highly rewarding for

those who can afford to wait.

Private

equity has outperformed public markets in 97 out of the last 100 quarters when

looking at 10-year rolling returns. Even during the three quarters of

underperformance, private equity regained its lead in the immediately following

quarter.

Robinhood’s European

Experiment

Tenev isn’t

just complaining about the problem. His company has already started testing

solutions, though not without controversy. Last month, Robinhood rolled out

tokenized products to European customers that supposedly give them exposure to

private companies like OpenAI without actually owning equity in those firms.

The move

raised eyebrows among regulators and industry watchers who questioned how these

products are valued and whether retail investors truly understand what they’re

buying. Critics worry about transparency and whether these complex instruments

could blow up in customers’ faces.

But Tenev

seems undeterred. “We’re obviously working to solve that,” he said,

suggesting more products could be coming to bridge the gap between retail

investors and private markets.

Robinhood

is not the only company currently offering such solutions. Several major

cryptocurrency exchanges have joined this trend as well, partnering with firms

like xStocks, which specializes in asset tokenization.

Why Private Markets May Be

Too Risky for Regular Investors

The

fundamental mismatch between how private markets operate and what everyday

investors need could create dangerous situations for both individuals and the

broader financial system.

The UK’s

Financial Conduct Authority delivered

a stark warning about this trend. Deputy Chief Executive Sarah Pritchard

emphasized that while some people might benefit from private market exposure

“with the right information and support,” the reality is that

“for others, it will not” be appropriate. The regulator’s position

acknowledges a harsh truth – these investments simply aren’t designed for most

people.

The core

problem lies in what experts call liquidity mismatch. Unlike stocks that you

can sell instantly, private market investments lock up your money for years

without any guarantee you can get it back when you need it. Moody’s research

highlighted this critical flaw: “Retail investors often require quicker

access to their capital and have less long-term investment flexibility”

compared to the pension funds and endowments that traditionally dominate these

markets.

Even more

troubling is what might happen if retail money floods into private markets too

quickly. Moody’s research suggests this could trigger a dangerous race among

fund managers to deploy capital, potentially leading them to “compromise

on underwriting standards or stretch into riskier assets to keep pace with

inflows.”

Wall Street Takes Notice

The private

markets boom has caught everyone’s attention, not just regulators and fintech

upstarts like Robinhood. Earlier this month, banking giants JPMorgan Chase and

Citigroup announced they’re expanding research coverage to include private

companies in hot sectors like artificial intelligence and aerospace.

The numbers

explain why. Private company valuations have been surging for years, creating

paper fortunes for those lucky enough to get in early. Meanwhile, the

traditional initial public offering market has struggled, with many companies

choosing to raise money privately rather than face the scrutiny of public

markets.

This trend

has created what Tenev calls the “greatest remaining iniquity” in

American finance. While pension funds, endowments, and wealthy individuals can

write checks to private equity firms and venture capital funds, regular

investors are largely shut out by regulations designed to protect them from

risky investments.

The Access Problem

The irony

isn’t lost on anyone. Robinhood made its name by eliminating trading

commissions and making it easier for millennials to buy stocks and options. But

when it comes to the investments that have generated the biggest returns over

the past decade, even Robinhood’s millions of users are stuck on the outside

looking in.

Current

regulations require investors to be “accredited” to participate in

most private investments, meaning they need either $1 million in net worth or

$200,000 in annual income. Those rules were written decades ago to protect

unsophisticated investors from losing their shirts on risky deals.

But critics

argue these outdated thresholds now serve mainly to protect the wealthy’s

access to the best investment opportunities. While a middle-class investor can

day-trade meme stocks on Robinhood, they can’t buy shares in the next big tech

startup.

“That’s

where I would point to as the greatest remaining iniquity and opportunity in

our capital markets,” Tenev said, making clear he sees this as more than

just a business opportunity for his company.

The

question now is whether regulators will go along with efforts to democratize

private markets, or whether they’ll stick with rules designed for a different

era of finance.

Robinhood’s

boss thinks there’s something fundamentally broken about how global capital

markets work. Vlad Tenev, the CEO who built his fortune democratizing stock

trading, now says it’s a “tragedy” that regular investors can’t

access private markets where the real money gets made.

Robinhood Boss Says Wall

Street’s Biggest Secret Is Unfair

Speaking on

Bloomberg

Wealth, Tenev didn’t mince words about what he sees as Wall Street’s

biggest inequity. “A big tragedy is that private markets are where the

bulk of the interesting appreciation and exposure is nowadays,” Robinhood’s Tenev told

host David Rubenstein. “It’s a shame that it’s so difficult to get

exposure in the US.”

The

comments highlight a growing frustration among retail trading platforms as

private companies stay private longer and capture more value before going

public. Companies like SpaceX, OpenAI, and other tech darlings have generated

massive returns for institutional investors while everyday Americans watch from

the sidelines.

What’s

important here, private market investments dramatically outperform public

markets over the long term, generating returns that can be 400-500 basis points

higher annually. The wealth creation difference is staggering – while public

market investors earned 6.6x their money over 25 years, private market

investors generated 19.9x returns according to Cambridge Associates’ comprehensive

data.

The Numbers Don’t Lie

Private

equity has delivered an average annual return of 13.1% over 25 years,

significantly outpacing the S&P 500’s 8.6% return during the same period.

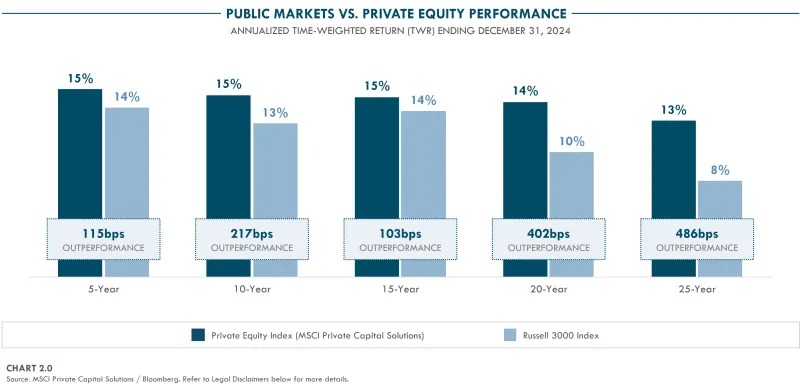

Even more

compelling data comes from MSCI Private Capital Solutions, which shows that

since 2000, private equity has generated a 13% net annualized return compared

to the Russell 3000’s 8% return. This represents outperformance of 486 basis

points annually.

The

illiquidity premium alone adds 2-4% annually to private equity returns over the

long run. This premium compensates investors for giving up the ability to sell

their investments quickly, but the trade-off has proven highly rewarding for

those who can afford to wait.

Private

equity has outperformed public markets in 97 out of the last 100 quarters when

looking at 10-year rolling returns. Even during the three quarters of

underperformance, private equity regained its lead in the immediately following

quarter.

Robinhood’s European

Experiment

Tenev isn’t

just complaining about the problem. His company has already started testing

solutions, though not without controversy. Last month, Robinhood rolled out

tokenized products to European customers that supposedly give them exposure to

private companies like OpenAI without actually owning equity in those firms.

The move

raised eyebrows among regulators and industry watchers who questioned how these

products are valued and whether retail investors truly understand what they’re

buying. Critics worry about transparency and whether these complex instruments

could blow up in customers’ faces.

But Tenev

seems undeterred. “We’re obviously working to solve that,” he said,

suggesting more products could be coming to bridge the gap between retail

investors and private markets.

Robinhood

is not the only company currently offering such solutions. Several major

cryptocurrency exchanges have joined this trend as well, partnering with firms

like xStocks, which specializes in asset tokenization.

Why Private Markets May Be

Too Risky for Regular Investors

The

fundamental mismatch between how private markets operate and what everyday

investors need could create dangerous situations for both individuals and the

broader financial system.

The UK’s

Financial Conduct Authority delivered

a stark warning about this trend. Deputy Chief Executive Sarah Pritchard

emphasized that while some people might benefit from private market exposure

“with the right information and support,” the reality is that

“for others, it will not” be appropriate. The regulator’s position

acknowledges a harsh truth – these investments simply aren’t designed for most

people.

The core

problem lies in what experts call liquidity mismatch. Unlike stocks that you

can sell instantly, private market investments lock up your money for years

without any guarantee you can get it back when you need it. Moody’s research

highlighted this critical flaw: “Retail investors often require quicker

access to their capital and have less long-term investment flexibility”

compared to the pension funds and endowments that traditionally dominate these

markets.

Even more

troubling is what might happen if retail money floods into private markets too

quickly. Moody’s research suggests this could trigger a dangerous race among

fund managers to deploy capital, potentially leading them to “compromise

on underwriting standards or stretch into riskier assets to keep pace with

inflows.”

Wall Street Takes Notice

The private

markets boom has caught everyone’s attention, not just regulators and fintech

upstarts like Robinhood. Earlier this month, banking giants JPMorgan Chase and

Citigroup announced they’re expanding research coverage to include private

companies in hot sectors like artificial intelligence and aerospace.

The numbers

explain why. Private company valuations have been surging for years, creating

paper fortunes for those lucky enough to get in early. Meanwhile, the

traditional initial public offering market has struggled, with many companies

choosing to raise money privately rather than face the scrutiny of public

markets.

This trend

has created what Tenev calls the “greatest remaining iniquity” in

American finance. While pension funds, endowments, and wealthy individuals can

write checks to private equity firms and venture capital funds, regular

investors are largely shut out by regulations designed to protect them from

risky investments.

The Access Problem

The irony

isn’t lost on anyone. Robinhood made its name by eliminating trading

commissions and making it easier for millennials to buy stocks and options. But

when it comes to the investments that have generated the biggest returns over

the past decade, even Robinhood’s millions of users are stuck on the outside

looking in.

Current

regulations require investors to be “accredited” to participate in

most private investments, meaning they need either $1 million in net worth or

$200,000 in annual income. Those rules were written decades ago to protect

unsophisticated investors from losing their shirts on risky deals.

But critics

argue these outdated thresholds now serve mainly to protect the wealthy’s

access to the best investment opportunities. While a middle-class investor can

day-trade meme stocks on Robinhood, they can’t buy shares in the next big tech

startup.

“That’s

where I would point to as the greatest remaining iniquity and opportunity in

our capital markets,” Tenev said, making clear he sees this as more than

just a business opportunity for his company.

The

question now is whether regulators will go along with efforts to democratize

private markets, or whether they’ll stick with rules designed for a different

era of finance.

This post is originally published on FINANCEMAGNATES.