A sharp slowdown in Swiss inflation and aggressive Fed rate cuts are prompting the Swiss National Bank to take decisive action. How will the USDCHF and EURCHF currency pairs react to the outcome of the September meeting? Let’s discuss this topic and make a trading plan.

The article covers the following subjects:

Highlights and key points

- The Fed’s aggressive start has the SNB hesitating.

- The SNB does not want deflation to return.

- Risks of a 50 bp key rate cut are growing.

- The EURCHF pair may soar to 0.98, and the USDCHF pair may slip to 0.82.

Weekly Swiss franc fundamental forecast

The market is structured in such a way that trends are replaced by consolidations, which in turn give way to new trends. The narrow trading range on the USDCHF pair is of particular interest, given the potential for an explosive breakout. The meeting of the National Bank is likely to be the catalyst for the breakout of one of the boundaries. The market is anticipating a bold move from the SNB, while economists are forecasting a more cautious approach. This is reminiscent of events on the eve of the September Fed meeting, which was followed by a significant market reaction.

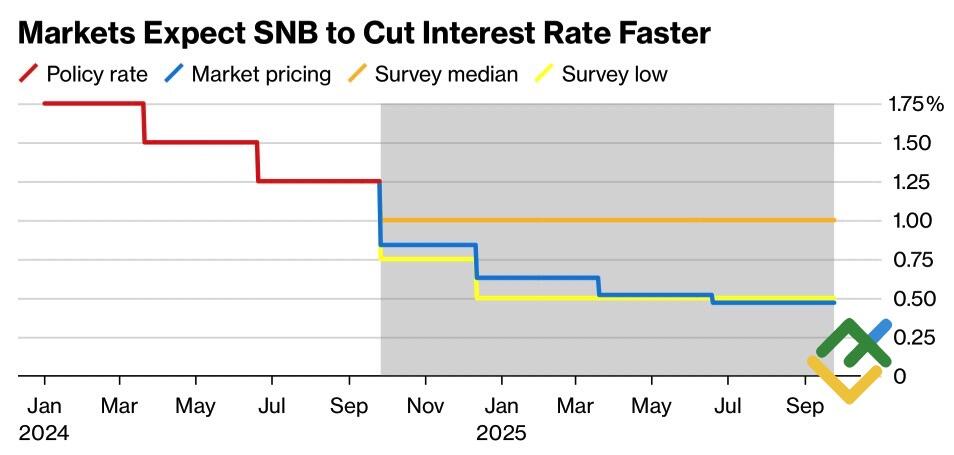

The Fed’s bold move has prompted analysts to speculate whether other central banks will follow suit. According to a survey conducted by Bloomberg, 29 out of 32 experts anticipate that the Swiss National Bank will reduce its key interest rate by 0.25 pp to 1% at its meeting on September 26. Meanwhile, there is one estimate that the central bank may cut the rate by half a point. Two respondents predict no change. In contrast, the futures market indicates that the SNB will continue to aggressively ease its monetary policy. Furthermore, the probability of this occurring has increased significantly since the Fed took decisive action at the outset of its monetary easing cycle.

SNB interest rate expectations

Source: Bloomberg.

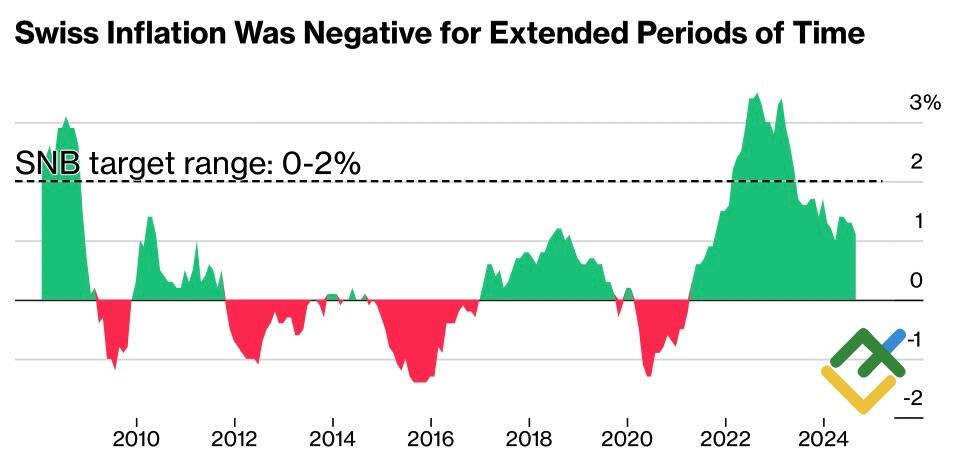

Given the limited availability of the National Bank’s resources, a cautious approach remains the optimal strategy. While there is currently no basis for reducing the key rate, a future opportunity may arise for a bold move. Inflation in Switzerland has decelerated, remaining within the target range of 0-2%. Centrists maintain that there is no immediate need for action.

Those with a dovish outlook believe that such a moment has come. The risk of a return to deflationary conditions, which has been a concern for the SNB since the beginning of the century up to 2021, is increasing. The decline in European business activity is prompting the ECB to consider loosening its monetary policy. If the Swiss central bank delays action, the franc will continue to appreciate against the currency of the region’s main trading partner, which will further slow the CPI and exacerbate exporters’ problems. The latter are already experiencing difficulties due to the strength of the Swiss franc.

Swiss inflation change

Source: Bloomberg.

Indeed, Thomas Jordan, who is stepping down as head of the SNB on September 30, may slam the door loudly on his way out of the office. Nevertheless, a drastic reduction in borrowing costs would effectively leave the SNB without the necessary resources. Should the Swiss economy slide into recession, the SNB will be forced to resort to the controversial practice of negative rates, which the central bank would prefer to avoid.

As might be expected, 16 of 32 Reuters experts believe that the key rate will end the year at 1%, 15 at 0.75%, and one at 1.25%. The current monetary expansion cycle is projected to conclude in March 2025 at 0.75%, after which no further adjustments are anticipated until 2026.

Weekly USDCHF and EURCHF trading plan

The probability of a 0.5% cut in borrowing costs in September is high. In this scenario, one can buy the EURCHF pair upon a breach of resistance at 0.9505, with projected targets of 0.9635 and 0.98. The anticipated 25-basis-point adjustment by the SNB has already been priced in the franc rate. Therefore, consider selling the USDCHF pair with the target of 0.82.

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2004/39/EC.

{{value}} ( {{count}} {{title}} )

This post is originally published on LITEFINANCE.